Income Tax Calculator India (FY 2024–25 to FY 2026–27)

Estimate your Indian income tax and compare Old Regime vs New Regime for FY 2024–25, FY 2025–26, and FY 2026–27 (standard deduction, rebate as implemented, surcharge, cess, special-rate income, and TDS/advance tax).

Tax Inputs

Rebate on ordinary income does not wipe out tax on special-rate income in this calculator.

Results

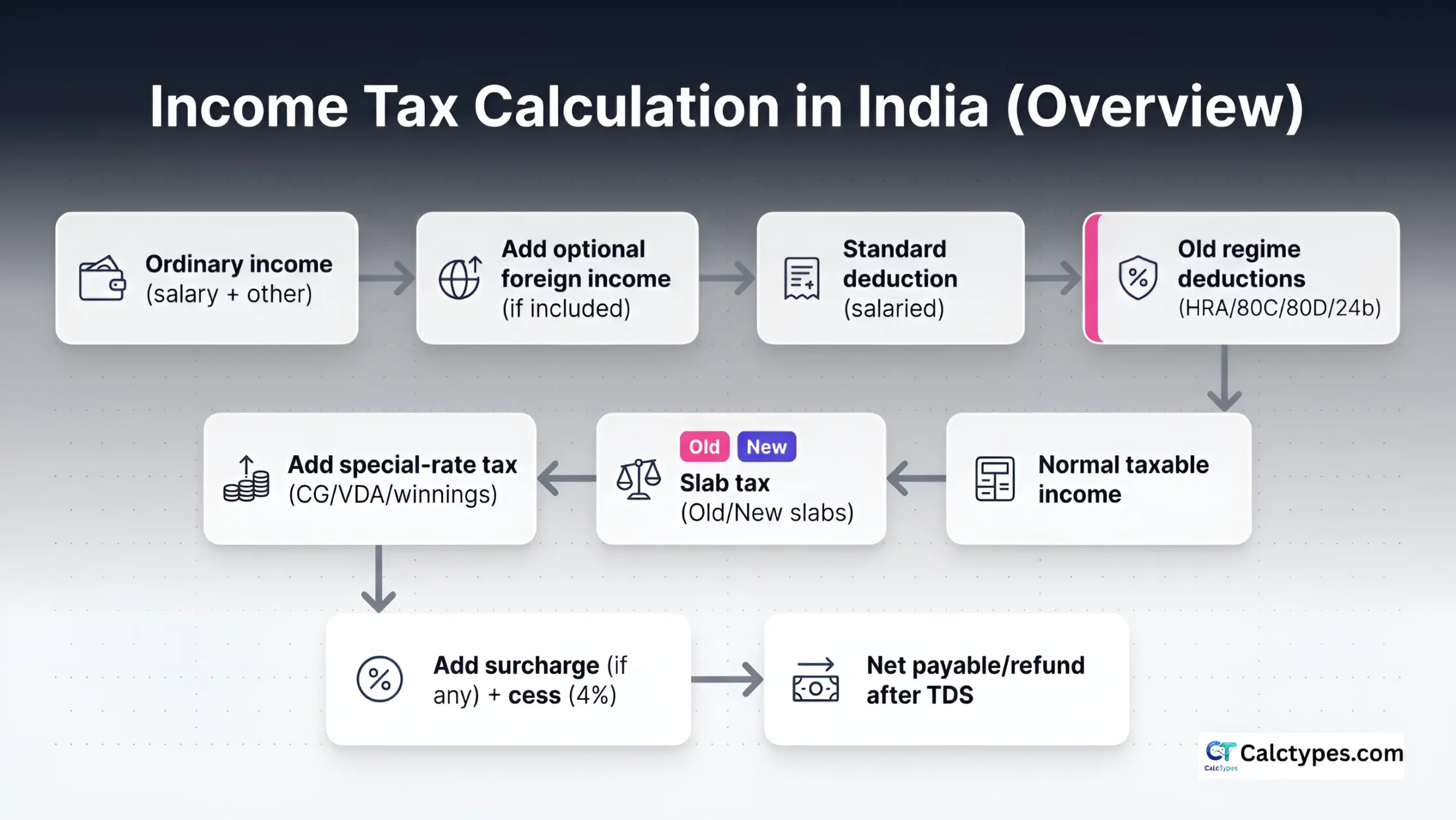

How this calculator computes your tax (quick steps)

- Compute ordinary income (India gross + other + optional foreign if included).

- Apply standard deduction (salaried only).

- Apply Old regime deductions (Old only): HRA exemption, 80C (capped), 80D, 24(b) (capped).

- Compute slab tax on normal taxable income.

- Add special-rate taxes (capital gains/VDA/winnings).

- Apply rebate against normal slab tax (if eligible in this tool).

- Apply surcharge (if applicable) + cess (4%).

- Net payable/refund = total tax − TDS/advance tax.

How your tax is calculated (based on your inputs)

Year: — · Residency: — · Income type: —

A) Income considered

- Ordinary income (incl. foreign if checked): —

- Old-regime deductions entered: —

- Special-rate income entered: —

B) Step-by-step (Old vs New)

| Step | Old Regime | New Regime |

|---|---|---|

| Standard deduction | — | — |

| Normal taxable income (slab base) | — | — |

| Slab tax on normal income (before rebate) | — | — |

| Rebate applied | — | — |

| Normal tax after rebate | — | — |

| Special-rate tax | — | — |

| Surcharge | — | — |

| Cess (4%) | — | — |

| Total tax | — | — |

| Net payable / refund (after TDS) | — | — |

C) Special-rate breakdown

- Enter special-rate income fields to see a breakdown here.

D) Result summary

Better regime: —

You save: —

Assumptions & Warnings

Share / Embed / Download

Old Regime vs New Regime (Chart)

Full Breakdown

| Item | Old Regime | New Regime |

|---|---|---|

| Enter your income to see the full breakdown. | ||

Income tax calculation in India (methodology used in this calculator)

- Ordinary income: India gross + other ordinary (+ optional foreign income if included).

- Standard deduction (salaried): applied per selected regime in this tool (capped at salary base).

- Old regime deductions (Old only): HRA exemption (input), 80C (capped), 80D, 24(b) (capped).

- Normal taxable income: max(0, ordinary income − standard deduction − old deductions (Old only)).

- Slab tax: computed using the selected year/regime slabs.

- Special-rate taxes: computed separately for STCG/LTCG/VDA/winnings at the configured rates.

- Rebate: applied only against normal slab-tax, not special-rate taxes (as implemented).

- Surcharge + marginal relief: applied where applicable (as implemented).

- Cess: 4% on (tax + surcharge).

- Net payable/refund: total tax − TDS/advance tax.

Related: Old vs New regime · Surcharge & cess

Income tax slabs (selected FY): New vs Old regime

Open this section to load the slab tables (keeps the page fast on mobile).

Guides: Slabs FY 2025–26 · Old vs New.

New Regime slab rates (auto-selected FY)

| New Regime — FY 2024–25 (AY 2025–26) | |

|---|---|

| ₹0 – ₹3,00,000 | 0% |

| ₹3,00,001 – ₹7,00,000 | 5% |

| ₹7,00,001 – ₹10,00,000 | 10% |

| ₹10,00,001 – ₹12,00,000 | 15% |

| ₹12,00,001 – ₹15,00,000 | 20% |

| Above ₹15,00,000 | 30% |

| New Regime — FY 2025–26 (AY 2026–27) | |

|---|---|

| ₹0 – ₹4,00,000 | 0% |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

| New Regime — FY 2026–27 / Tax Year 2026–27 | |

|---|---|

| ₹0 – ₹4,00,000 | 0% |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

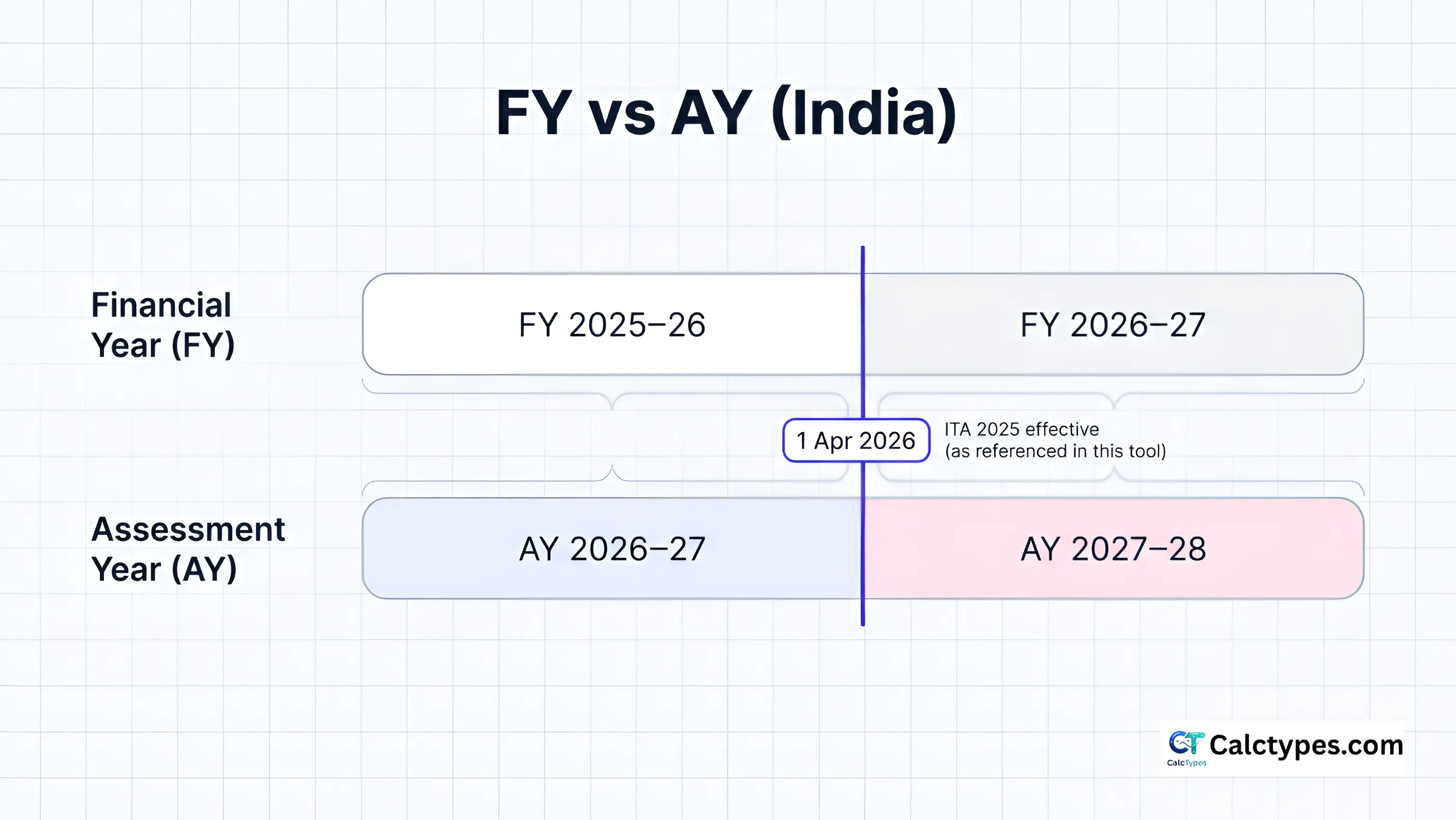

FY 2026–27 shown under ITA 2025 framework as implemented in this calculator.

Old Regime slab rates (by age)

| Age category | Income slab | Rate |

|---|---|---|

| Under 60 | ₹0 – ₹2,50,000 | 0% |

| ₹2,50,001 – ₹5,00,000 | 5% | |

| ₹5,00,001 – ₹10,00,000 | 20% | |

| Above ₹10,00,000 | 30% | |

| Senior (60–79) | ₹0 – ₹3,00,000 | 0% |

| ₹3,00,001 – ₹5,00,000 | 5% | |

| ₹5,00,001 – ₹10,00,000 | 20% | |

| Above ₹10,00,000 | 30% | |

| Super senior (80+) | ₹0 – ₹5,00,000 | 0% |

| ₹5,00,001 – ₹10,00,000 | 20% | |

| Above ₹10,00,000 | 30% |

Cess: 4% on (tax + surcharge). More: surcharge & cess guide.

Worked examples (detailed) — compare Old vs New

Open this section to load the worked examples tables.

Example 1 (FY 2025–26): Salary ₹12,75,000, Resident, Salaried, low deductions

This highlights why “~₹12.75L salary” can show zero normal slab tax under the New regime (as implemented here).

| Step | New Regime |

|---|---|

| Gross salary | ₹12,75,000 |

| Standard deduction (New) | ₹75,000 |

| Normal taxable income | ₹12,00,000 |

| Normal slab tax (before rebate) | ₹60,000 |

| Rebate (as implemented for eligible residents) | ₹60,000 |

| Cess | ₹0 |

| Total tax | ₹0 |

Example 2 (FY 2025–26): Salary ₹18,00,000 with high Old deductions

Example Old deductions entered: HRA ₹3,00,000 + 80C ₹1,50,000 + 80D ₹50,000 + 24(b) ₹2,00,000 (caps applied).

| Step | Old Regime | New Regime |

|---|---|---|

| Gross salary | ₹18,00,000 | ₹18,00,000 |

| Standard deduction | ₹50,000 | ₹75,000 |

| Old deductions (HRA+80C+80D+24b) | ₹7,00,000 | N/A |

| Normal taxable income | ₹10,50,000 | ₹17,25,000 |

Verdict: Old may win when deductions are large. Always verify with your exact values.

Example 3 (FY 2025–26): Salary within rebate, but LTCG pushes total income above the limit

Inputs (New Regime): Gross salary ₹12,75,000 (normal taxable ₹12,00,000) + LTCG (equity) ₹2,50,000. In this calculator’s implementation, rebate eligibility uses total taxable income, so adding special-rate income can remove the rebate.

| Component | New Regime |

|---|---|

| Normal taxable income | ₹12,00,000 |

| Normal slab tax (before rebate) | ₹60,000 |

| LTCG equity taxable (after ₹1,25,000 threshold) | ₹1,25,000 |

| LTCG equity tax (12.5%) | ₹15,625 |

| Rebate impact | May not apply because total taxable income exceeds ₹12,00,000 (as implemented) |

| Total tax (approx, incl. cess) | ₹78,650 |

Questions people ask

Common questions about Indian income tax and how this calculator models it.

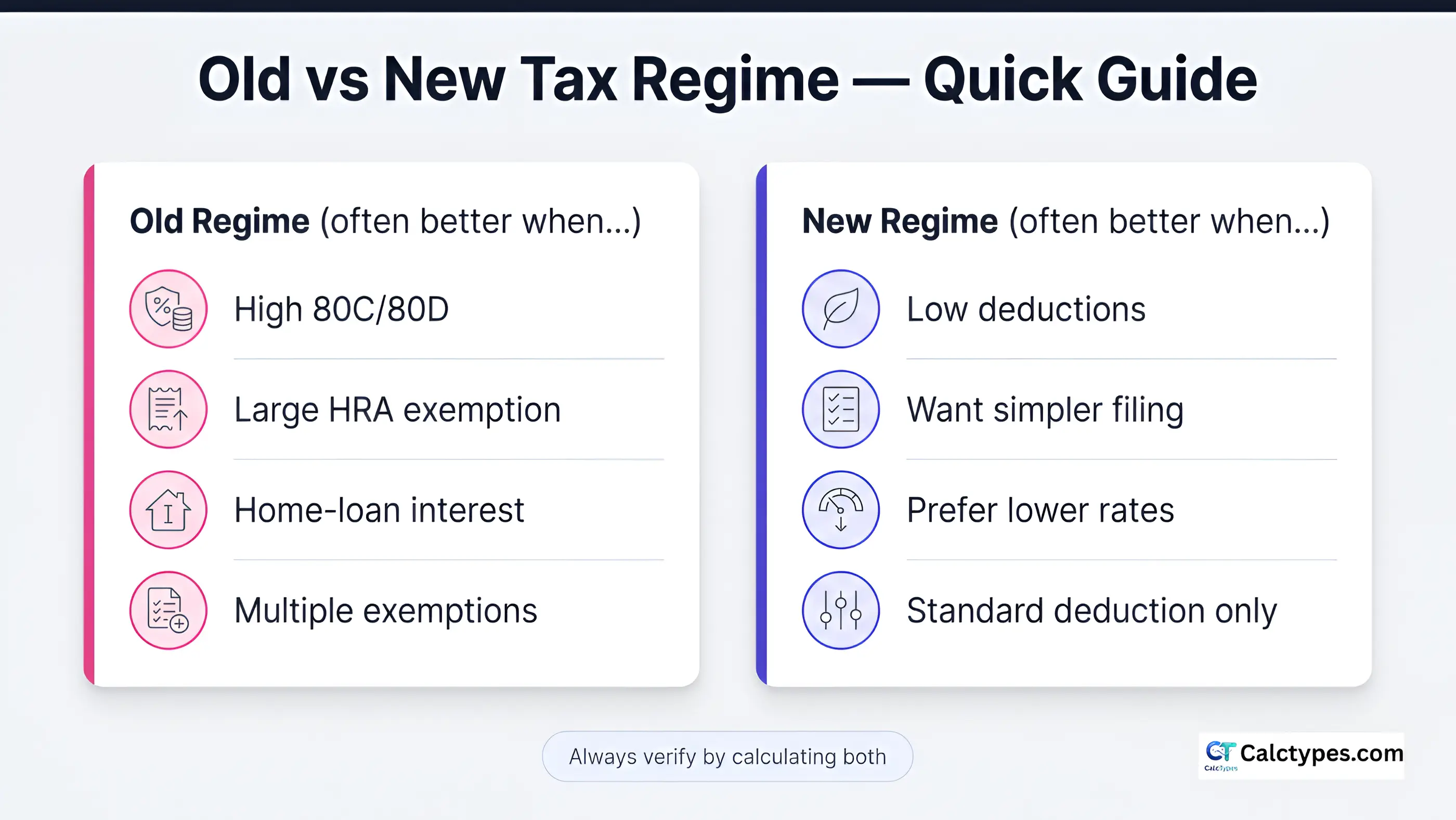

Which tax regime is better — Old or New?

It depends on your deductions. If you claim large deductions/exemptions (like 80C, 80D, HRA, and home-loan interest), the Old Regime can be better. If your deductions are low, the New Regime often reduces tax. Use the calculator to compare both for your year and inputs.

What is the maximum salary with zero tax under the New Regime for FY 2025–26?

In this calculator, a gross salary of about ₹12,75,000 can show zero normal slab-tax under the New Regime for FY 2025–26, because after the ₹75,000 standard deduction the normal taxable income becomes ₹12,00,000 (eligible for rebate as implemented for resident-like users).

Why is my tax not zero even though my income seems within the rebate?

Two common reasons in this calculator: (1) you have special-rate income (capital gains, VDA, winnings) which is added separately and not wiped out by rebate, and/or (2) special-rate income can push your total taxable income above the rebate limit (as implemented), removing the rebate.

Does my age affect my slabs?

Age affects slab thresholds only under the Old Regime (and only for the resident-like handling in this tool). New Regime slabs are the same for all ages.

Are NRIs eligible for the rebate in this calculator?

No. If you choose Non-Resident (NRI), rebate is not applied in this tool.

Does this calculator include surcharge and marginal relief?

Yes, it applies surcharge for higher total incomes and uses a basic marginal-relief mechanism on surcharge thresholds (as implemented). Cess is applied at 4%.

How are stock and mutual fund capital gains taxed here?

- STCG (equity/units with STT): 20%

- LTCG equity (STT-paid): 12.5% on gains above ₹1,25,000 (annual threshold used in this calculator)

- Other LTCG: 12.5%

These are computed separately and added to your normal slab tax in this tool.

What deductions do I lose if I choose the New Regime?

Typically, popular Old-regime deductions/exemptions are not used in the New Regime calculation, such as:

- 80C (up to ₹1.5L)

- 80D (health insurance premiums)

- HRA exemption

- Home-loan interest under 24(b) (as modeled here)

What is FY vs AY?

FY is the year you earn income. AY is the year you file tax return for that FY. The dropdown shows FY and the corresponding AY label.

Sources & Further Reading

These links support slab rates, rebate references, and special-rate provisions. Always verify on the official portal or consult a qualified CA before filing.

- Income Tax Department — Official Portal (rules, filing, official references)

- Income Tax Department — Official Tax Calculator (cross-check estimates)

- Finance Bill / Budget Documents (slab/rebate changes)

- Income Tax Department — Section 115BB (winnings) (special-rate winnings)

- Income-tax Act, 2025 (reference) (FY 2026–27 note)

- Income-tax Act, 1961 (reference) (earlier years)

Disclaimer: This page provides an educational estimate only and is not tax advice.

Important Disclaimer

This calculator provides a general educational estimate based on the inputs you enter and the assumptions implemented in this tool. It is not tax advice and should not be relied on for filing, compliance, or any legal/financial decision. Tax outcomes can differ due to rules not captured here (deductions/exemptions, set-off/carry-forward, special provisions, rounding, DTAA/FTC, regime eligibility rules, amendments/notifications, etc.). Always verify using the official Income Tax Department tools and/or consult a qualified Chartered Accountant. Read full disclaimer.